Let me be straight with you: if you’re thinking about becoming a loan officer, most of what you’ll hear about salaries is either outdated or flat-out misleading.

I’ve been in this industry long enough to see people get excited about a $60,000 “salary” only to realize that’s just the base – and your real income depends on how many loans you close. Others walk away from great opportunities because they got scared by the commission structure without understanding how it actually works.

With employment of loan officers projected to grow 2 percent from 2024 to 2034 according to the Bureau of Labor Statistics, this field continues to offer opportunities despite slower-than-average growth. But here’s what they don’t mention: the people who figure out this compensation game can make serious money.

Table of Contents

-

The Real Numbers (No BS)

-

Where You Work Matters More Than You Think

-

How Commission Actually Works

-

The Career Path Nobody Explains

-

What Actually Drives Your Paycheck

-

Market Conditions and Your Income

-

Professional Development That Pays

-

Your Action Plan for Maximum Earnings

TL;DR

-

Base salaries are just the starting point – commission often doubles or triples your total income

-

Location dramatically affects your purchasing power, not just your paycheck

-

Top performers convert 40-60% of applications while average loan officers struggle at 25-35%

-

Specialization in commercial or jumbo loans can boost your income by 20-40%

-

Independent brokers have the highest earning potential but take on more risk

-

Strong referral networks generate 30-50% of business for established loan officers

-

Technology skills can increase your performance by 25-40% over peers who ignore digital tools

The Real Numbers (No BS)

Forget everything you’ve heard about loan officer salaries. Here’s what actually happens:

Your first year: $35,000-$55,000 (mostly base salary while you learn)

Years 2-5: $60,000-$100,000 (commission kicks in as you build relationships)

Experienced pros: $100,000-$200,000+ (commission becomes your main income)

Top performers: $200,000-$300,000+ (usually independent brokers)

But here’s the catch – location changes everything, and recent regulatory developments are reshaping the entire compensation landscape. In June, the Consumer Financial Protection Bureau submitted a proposed rulemaking that could significantly amend current Loan Originator Compensation rules. If enacted, this change could remove long-standing restrictions on LO compensation, giving lenders more flexibility in designing pay structures.

What The Industry Actually Pays

Most loan officers start with base salaries between $40,000-$80,000, but this is just the foundation. The real money comes from understanding how commission structures work and positioning yourself to maximize them.

Professional credibility plays a crucial role in establishing trust with clients and commanding higher compensation. When potential borrowers evaluate your expertise, they often look for visible indicators of your qualifications, including properly displayed educational credentials that reinforce your professional standing in the competitive lending industry.

|

Experience Level |

Base Salary Range |

Total Compensation Range |

Primary Income Source |

|---|---|---|---|

|

Entry-Level (0-2 years) |

$35,000-$45,000 |

$35,000-$55,000 |

Base salary + minimal commission |

|

Mid-Career (3-7 years) |

$45,000-$65,000 |

$60,000-$100,000 |

Balanced base + commission |

|

Senior-Level (8+ years) |

$55,000-$80,000 |

$100,000-$200,000+ |

Commission-heavy structure |

|

Management/Independent |

$60,000-$90,000 |

$150,000-$300,000+ |

Commission + overrides/equity |

The reality is that how much a loan officer makes depends heavily on their ability to generate commission income beyond their base salary. I’ve seen too many new loan officers focus solely on base salary numbers during job interviews, completely missing the bigger picture of total earning potential.

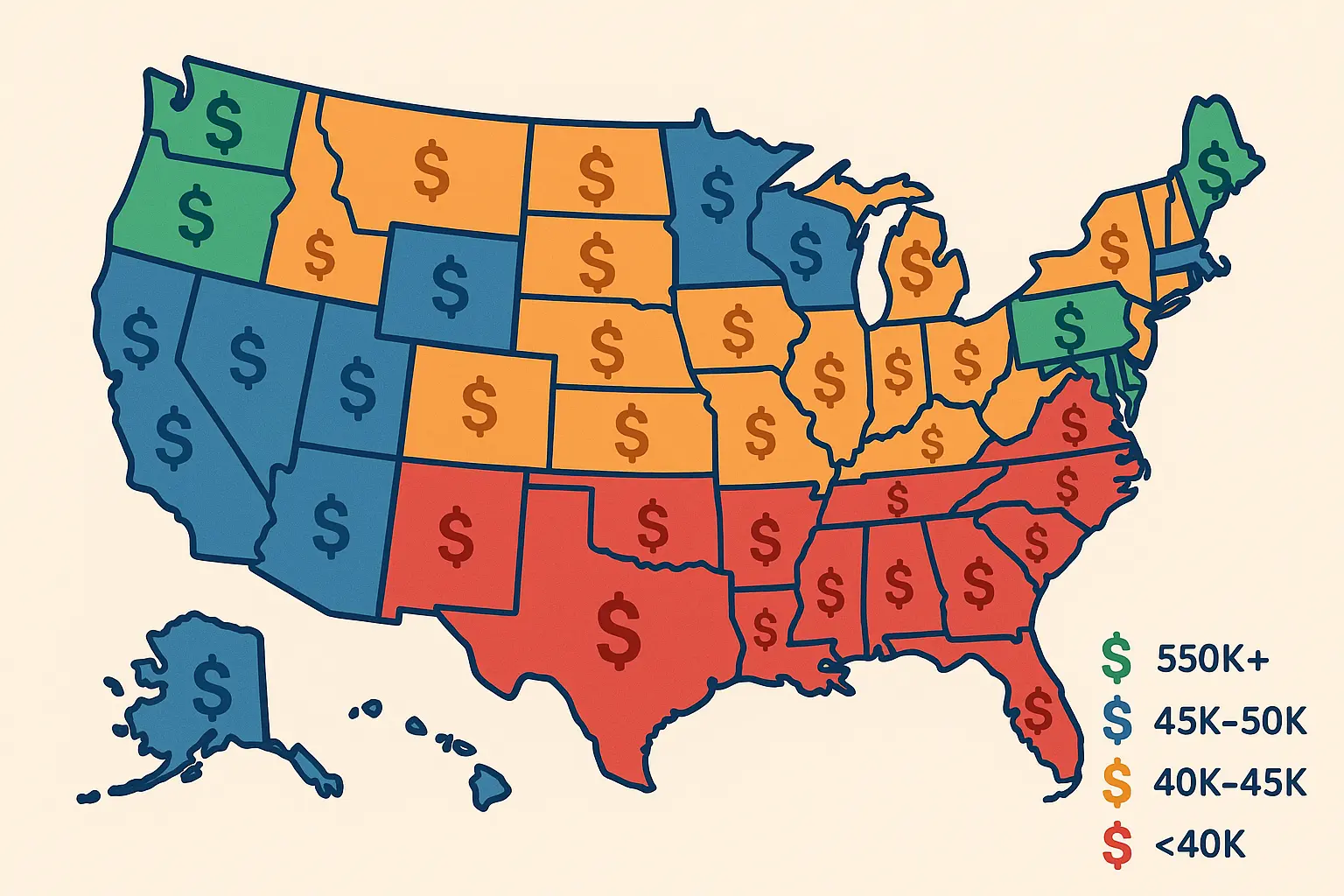

Where You Work Matters More Than You Think

I’ve seen loan officers make $150,000 in California and struggle to pay rent, while others earn $75,000 in Ohio and live like kings. Location doesn’t just affect your salary – it determines your actual purchasing power and quality of life.

High-salary, high-cost areas:

– California: $85,000-$150,000 (but you’ll spend 45-55% on housing)

– New York: $110,000-$130,000 (40-50% goes to housing)

Better purchasing power:

– Texas: $75,000-$95,000 (only 25-30% for housing)

– Midwest: $60,000-$75,000 (20-25% for housing)

The math is simple: would you rather make $150,000 and spend $75,000 on housing, or make $75,000 and spend $18,000?

West Coast vs Midwest Reality Check

California leads national compensation with average total earnings of $85,000-$150,000, driven by high property values and substantial lending volume. But when you factor in living costs, those impressive numbers lose their shine fast.

Meanwhile, Ohio and Michigan markets offer strong purchasing power despite lower nominal salaries. These regions provide opportunities to build wealth more effectively due to lower housing costs and living expenses.

|

Market Region |

Average Total Compensation |

Cost of Living Index |

Purchasing Power Score |

Housing Cost % of Income |

|---|---|---|---|---|

|

California (Bay Area) |

$125,000-$150,000 |

180-200 |

6.5/10 |

45-55% |

|

New York Metro |

$110,000-$130,000 |

170-190 |

6.0/10 |

40-50% |

|

Texas (Dallas/Houston) |

$75,000-$95,000 |

95-105 |

8.5/10 |

25-30% |

|

Florida (Miami/Tampa) |

$70,000-$90,000 |

105-115 |

7.5/10 |

30-35% |

|

Midwest (Ohio/Michigan) |

$60,000-$75,000 |

85-95 |

8.0/10 |

20-25% |

How Commission Actually Works

This is where most people get confused. Commission isn’t just “extra money” – for experienced loan officers, it’s usually 60-80% of their total income.

Here’s a real example: Sarah closes $2 million in loans monthly at 1% commission. That’s $20,000 per month in commission alone ($240,000 annually), on top of her $50,000 base salary.

Typical commission structure:

– 0.5-2% of loan amount

– Higher rates for complex loans (jumbo, commercial)

– Bonuses for approval rates and customer satisfaction

The key insight? Volume matters, but so does quality. Chase volume without caring about approvals, and you’ll lose bonus money fast.

Volume-Based vs Quality-Based Earnings

Loan officers typically earn between 0.5-2% commission on total loan amounts, with higher percentages available for complex transactions or high-value loans. But smart loan officers know that additional compensation tied to loan approval rates, customer satisfaction scores, and portfolio performance can significantly boost total earnings.

I’ve worked with loan officers who initially chased volume at the expense of quality, only to see their bonus compensation suffer. The smart ones quickly learned that maintaining high approval rates and customer satisfaction scores creates a more sustainable income stream.

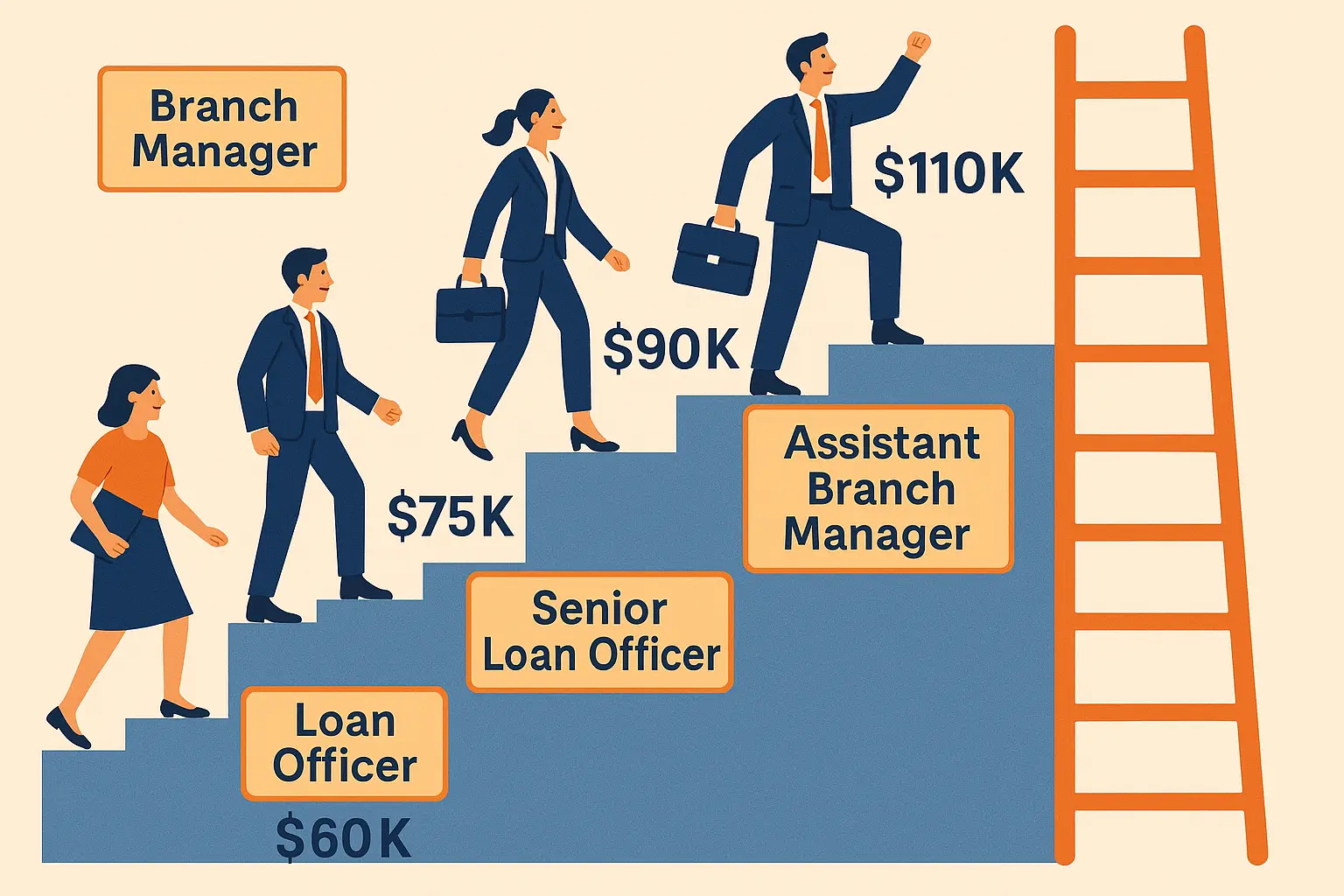

The Career Path Nobody Explains

Career advancement in the lending industry often requires demonstrating educational qualifications and professional achievements. Many loan officers find that pursuing higher education credentials can open doors to management positions and specialized roles that command significantly higher compensation packages.

Months 1-6: Training mode

You’re basically getting paid to learn. Most companies guarantee your base salary during training, usually $35,000-$45,000. Use this time to absorb everything.

New Loan Officer Onboarding Checklist:

– Complete NMLS licensing requirements and background check

– Attend company-specific training program (3-6 months)

– Shadow experienced loan officers for 30-60 days

– Learn CRM and loan origination software systems

– Establish relationships with key referral partners

– Set up personal marketing materials and social media presence

– Complete first 10 loan applications under supervision

– Achieve initial performance benchmarks for commission eligibility

The loan officer salary during training might seem modest, but I always tell new hires to view this as an investment in their future earning potential. The skills you develop during this period directly impact your ability to generate commission income later.

Years 1-2: Building your foundation

This is the hardest part. You’re developing skills and relationships while earning mostly base salary. Many people quit here because they expect immediate big money.

Years 3-7: The sweet spot

Your referral network starts paying off. You understand the systems. Commission becomes significant. This is where $60,000-$100,000 becomes realistic.

Mike specialized in VA loans after his military service and now earns 30% more than his residential counterparts. His military background helps him connect with veteran borrowers, and his specialized knowledge allows him to handle complex VA transactions that other loan officers refer out. This specialization has increased his average commission from 0.75% to 1.1% per loan.

Years 8+: Senior level decisions

You can stay as a high-earning individual contributor, move into management, or go independent. Each path has different income potential and risks.

What Actually Drives Your Paycheck

The mortgage industry is currently facing significant compliance challenges that directly impact loan officer compensation. A recent class-action lawsuit against loanDepot alleges violations of federal loan officer compensation rules, including steering borrowers into higher-rate loans and falsifying documentation. These cases highlight the importance of understanding and adhering to compensation regulations while building sustainable income streams.

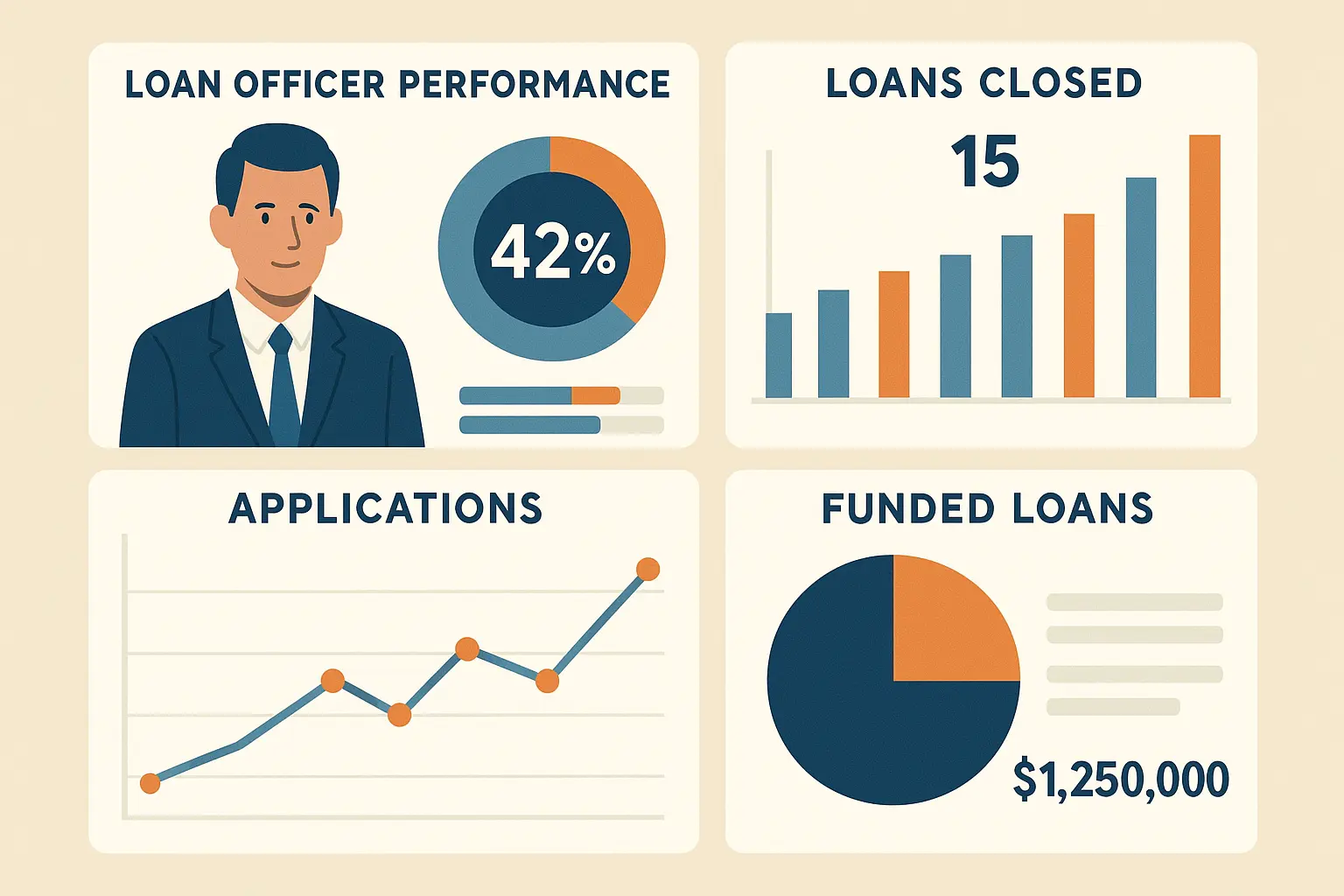

Here’s the reality check nobody gives you: your income isn’t just about closing loans. It’s about understanding the metrics that employers actually track.

The Numbers That Matter

Pipeline management is everything. You need 3-4 applications in your pipeline for every loan you want to close. Here’s how the timeline works:

– Weeks 1-2: Get the application and documents

– Weeks 3-4: Submit to underwriting, clear conditions

– Weeks 5-6: Final approval and prep for closing

– Weeks 7-8: Close and fund

Most new loan officers focus on getting applications but ignore pipeline management. That’s why their income is all over the place.

Conversion rates separate the pros from everyone else. Industry average is 25-35%, but top earners convert 40-60% of applications.

Jennifer figured this out the hard way. She was getting 20 applications monthly but only closing 6 loans (30% conversion). She revamped her follow-up process and qualification procedures. Now she closes 10 loans from the same 20 applications – a 67% income increase without generating more leads.

The Referral Game

Once you’re established, 30-50% of your business should come from referrals. This isn’t just about being nice to clients – it’s about systematic relationship building:

Professional Network Building Checklist:

– Join local real estate investment groups and networking organizations

– Attend monthly realtor office meetings and market updates

– Establish partnerships with 5-10 high-producing real estate agents

– Connect with financial planners, CPAs, and estate attorneys

– Participate in community events and charitable organizations

– Maintain active LinkedIn presence with weekly industry content

– Schedule quarterly coffee meetings with key referral partners

– Track referral sources and ROI for relationship investments

Building these relationships takes time, but the loan officer salary increases that result from consistent referral business make the investment worthwhile. I’ve watched loan officers double their income simply by focusing on relationship building rather than cold calling.

Market Conditions and Your Income

The mortgage industry runs in cycles, and smart loan officers adapt their strategy accordingly.

Interest Rate Reality

When rates are low: Everyone refinances. Easy money, high volume, lots of competition.

When rates rise: Only serious buyers apply. Harder work, fewer deals, but less competition.

Refinance specialists make bank when rates drop but struggle when they rise. Purchase specialists have steadier income but work harder for each deal.

The smart play? Learn both, but know which market you’re in.

Economic Cycles

Recessions actually create opportunities for experienced loan officers. While overall volume drops, weaker competitors leave the market. If you’ve built solid relationships and understand complex loan products, you can gain market share.

Professional Development That Pays

When pursuing career advancement opportunities, professionals sometimes need to provide proof of their educational background. If you’ve lost or damaged important credentials, understanding the process for replacing lost diplomas ensures you can quickly restore your professional documentation without missing critical career opportunities.

Most loan officers stop learning after they get licensed. That’s a mistake.

Certifications Worth Your Time

-

CML (Certified Mortgage Lender): 10-15% income boost

-

CRCM (Certified Regulatory Compliance Manager): Opens doors to management

-

Specialized designations: VA, FHA, USDA expertise pays premium rates

Technology Skills

This is huge and most people ignore it. Loan officers who master CRM systems and digital marketing consistently out-earn peers by 25-40%.

Essential tech stack:

– CRM system (for lead nurturing)

– Social media marketing (LinkedIn is gold)

– Email automation

– Digital application systems

– Video conferencing tools

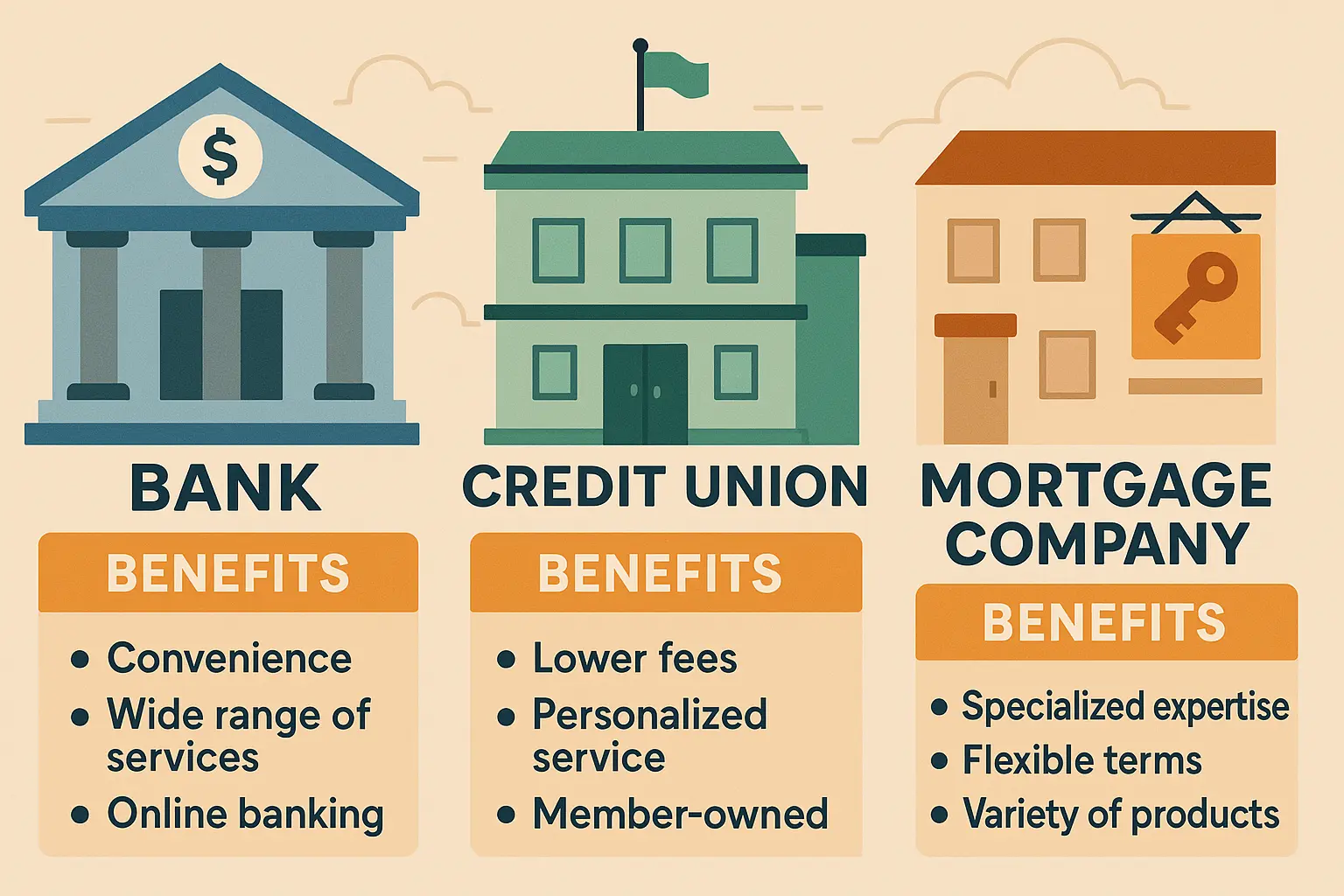

Industry Sectors: Where to Work

Employment setting significantly impacts compensation structure, benefits packages, and long-term growth opportunities.

Big Banks

-

Higher base salaries ($50,000-$90,000)

-

Aggressive commission structures

-

Great training programs

-

High performance pressure

Credit Unions

-

Steady salaries ($45,000-$70,000)

-

Better benefits

-

More job security

-

Emphasis on relationships over volume

Independent Mortgage Companies

-

Highest earning potential ($200,000+)

-

Pure commission structures

-

More freedom, more risk

-

You handle your own business development

Independent Brokerage

-

Unlimited earning potential

-

Keep larger commission percentages

-

Handle all business expenses

-

Requires entrepreneurial skills

Your Action Plan for Maximum Earnings

Professional presentation matters significantly in the financial services industry, and many successful loan officers find that displaying their educational achievements prominently helps build client trust. Learning effective ways to display certificates and diplomas can enhance your office’s professional appearance and reinforce your qualifications to potential borrowers.

Here’s your roadmap to higher income:

Year 1-2: Foundation Building

-

Complete NMLS licensing

-

Choose your employer based on training quality, not just commission rates

-

Focus on learning systems and building initial relationships

-

Track everything: lead sources, conversion rates, what works

Year 3-5: Scaling Up

-

Develop your specialization (commercial, jumbo, government loans)

-

Build strategic partnerships with real estate agents

-

Implement systematic follow-up processes

-

Target 15-25% income increases every 2-3 years

Year 5+: Strategic Decisions

-

Consider management roles (additional $10,000-$25,000)

-

Evaluate independent brokerage opportunities

-

Expand into related services (insurance, financial planning)

-

Mentor junior loan officers for override income

The Geographic Strategy

Don’t just look at salary numbers – look at purchasing power.

Best markets for purchasing power:

– Texas (Dallas/Houston): $75,000-$95,000 salary, 25-30% housing costs

– Florida: $70,000-$90,000 salary, 30-35% housing costs

– Midwest: $60,000-$75,000 salary, 20-25% housing costs

High salary, questionable value:

– California: $125,000-$150,000 salary, but 45-55% goes to housing

– New York: $110,000-$130,000 salary, but 40-50% goes to housing

Warning Signs and Red Flags

Bad employers:

– Unclear commission structures

– High turnover rates

– Unrealistic volume expectations for new hires

– All commission, no base salary (unless you’re experienced)

Market warning signs:

– Rapidly rising interest rates

– Local economic downturns

– Oversaturated markets

– New regulatory changes

The Real Success Formula

After watching hundreds of loan officers over the years, here’s what separates the $200,000+ earners from everyone else:

-

They specialize: Generic loan officers are replaceable

-

They build systems: Consistent follow-up, pipeline management, lead nurturing

-

They focus on relationships: Long-term thinking beats short-term volume chasing

-

They adapt to markets: Rising rates? They pivot to purchase loans. Recession? They focus on quality over quantity

-

They never stop learning: Technology, regulations, market trends

Your Next Steps

If you’re starting out:

– Get licensed immediately

– Research employers based on training quality and realistic income expectations

– Choose your geographic market strategically

– Plan your specialization within 2-3 years

If you’re already working:

– Audit your current performance metrics

– Identify your weakest area (lead generation, conversion, or follow-up)

– Build one new strategic relationship monthly

– Track your numbers obsessively

Final Thoughts

Your success as a loan officer depends on understanding the complete compensation picture and taking strategic action to maximize your earning potential. The lending industry rewards those who combine relationship-building skills with business acumen and market awareness.

Building a successful loan officer career requires more than just understanding salary ranges – it demands strategic thinking about your professional image and credibility. When clients walk into your office, they’re making split-second judgments about your competence and trustworthiness based on what they see. If you need to replace educational credentials for professional display, understanding the diploma replacement process can help you maintain that polished, credible appearance that’s essential in financial services.

Your educational credentials play a crucial role in establishing that professional credibility. If you’ve lost or damaged your diploma, or need a backup copy for your office while keeping the original secure, ValidGrad can help you create a professional replacement for display purposes. Having your educational achievements prominently displayed builds client confidence and demonstrates your qualifications in a competitive industry.

The loan officer game rewards those who understand it’s not just about sales – it’s about building a sustainable business based on relationships, expertise, and systematic processes. Your income ceiling is largely up to you. The question is whether you’re willing to do the work that most loan officers won’t do.

ValidGrad’s diploma maker offers fast turnaround and quality materials, ensuring you can quickly restore your professional appearance and continue focusing on what matters most – helping clients and maximizing your earning potential. Don’t let a missing or damaged diploma undermine the professional image you’ve worked hard to build.