The loan signing agent profession presents a fascinating income paradox that most people never fully understand. While ZipRecruiter reports that the majority of Loan Signing Agent salaries currently range between $27,874 (25th percentile) to $56,677 (75th percentile) with top earners (90th percentile) making $84,551 annually in Arizona, the reality is far more complex than these broad statistics suggest.

I’ve spent years in this industry, and I can tell you the difference between struggling agents and those earning six figures often comes down to understanding market dynamics, strategic positioning, and hidden cost management that most loan signing agent professionals never learn. The income potential exists, but you need to know where to look and how to position yourself.

Table of Contents

- Why Your Location Determines Your Paycheck More Than Your Skills

- The Service Upgrades That Command Premium Rates

- Hidden Costs That Are Secretly Killing Your Profits

- Multiple Income Streams Beyond Basic Signings

- Technology That Actually Increases Your Hourly Rate

- Timing the Market for Maximum Annual Earnings

- How Professional Credibility Impacts Your Fee Negotiations

- Final Thoughts

TL;DR

- Geographic positioning can increase your per-signing rate by 30-50% – rural areas often pay premium rates due to limited agent availability

- After-hours and specialized services (commercial loans, reverse mortgages) can command $200-500 per signing versus $75 for standard appointments

- Hidden costs like vehicle depreciation and time inefficiencies can reduce your effective hourly rate by 40-60%

- Top urban agents earn $75,000-120,000 annually through volume optimization and relationship building

- Technology investments of $2,000-5,000 can dramatically improve productivity and justify premium pricing

- Seasonal market timing allows smart agents to earn 40-60% of annual income during peak months

- Professional documentation and credibility directly impact your ability to negotiate higher fees

Why Your Location Determines Your Paycheck More Than Your Skills

I learned this lesson the hard way when I first started as a loan signing agent. I was focused on perfecting my technique and getting faster at document reviews, thinking skills would determine my income. Wrong. Where you work matters more than how well you work, at least when it comes to base rates.

Geographic positioning creates dramatic income disparities within the loan signing profession that most agents never fully understand. Rural markets often pay 30-50% premium rates due to limited competition, while urban areas reward high-volume efficiency. The key is understanding market density, competition saturation, and how title companies value reliable service in different locations.

When people ask me how much does a notary make, I always start with location because it’s the biggest factor. A loan signing agent in rural Montana can earn more per signing than someone in downtown Los Angeles, even though the LA agent might handle triple the volume.

| Market Type | Average Per-Signing Rate | Competition Level | Volume Potential | Travel Requirements |

|---|---|---|---|---|

| Rural/Remote | $150-$250 | Low | 5-15 signings/month | High (30+ miles) |

| Suburban | $125-$200 | Moderate | 15-40 signings/month | Moderate (10-20 miles) |

| Urban | $75-$150 | High | 40-100+ signings/month | Low (5-15 miles) |

| Metropolitan | $100-$175 | Very High | 60-120+ signings/month | Variable |

The Rural Premium That Most Agents Miss

Remote and semi-rural markets consistently offer higher per-signing rates because fewer agents are willing to travel these distances. While urban agents compete on price, rural specialists can command premium rates of $150-250 per signing due to limited availability and higher travel requirements.

I know this sounds counterintuitive. You’d think cities would pay more, right? But title companies in rural areas have fewer reliable options, and they’re willing to pay for dependability.

Why Remote Areas Pay More (And How to Capitalize)

Rural markets pay premium rates because title companies have fewer reliable options and borrowers often have limited scheduling flexibility. Agents who position themselves as the go-to professional for outlying areas can build sustainable businesses with higher per-signing income, though at lower overall volume.

Sarah, a loan signing agent in rural Montana, discovered that by positioning herself as the specialist for remote ranch properties and small towns within a 75-mile radius, she could command $200-275 per signing. While she only completes 12-18 signings monthly, her annual income of $65,000 exceeds many urban agents handling 60+ signings at lower rates. Her secret: becoming the reliable go-to professional for three title companies serving remote areas where other agents won’t travel.

The math works because you’re solving a real problem. Title companies need someone they can count on, and borrowers in remote areas can’t easily reschedule if you don’t show up.

Urban Volume vs. Suburban Relationships

Metropolitan markets operate on fundamentally different economics than suburban areas. Urban success depends on completing 3-4 signings daily through route optimization and maintaining 15+ active title company relationships, while suburban markets reward relationship-building and consistent quality service.

I’ve worked both markets, and they require completely different mindsets. Urban work feels more like logistics management, while suburban work is relationship-driven.

High-Volume Urban Strategies That Actually Work

Urban agents earning $75,000-120,000 annually master efficiency systems including geographic clustering, automated scheduling, and maintaining relationships with multiple signing services. Success requires treating the work as a logistics business rather than individual appointments.

The loan signing agent professionals who thrive in cities think systematically. They don’t just take whatever appointments come their way – they optimize for efficiency and volume.

Urban Agent Success Checklist:

- Maintain active relationships with 15+ title companies

- Develop geographic clustering system for appointments

- Implement automated scheduling and route optimization

- Target 3-4 signings per day during peak periods

- Build backup systems for equipment and transportation

- Create standardized pricing for different service levels

- Establish emergency coverage network with other agents

The Suburban Sweet Spot for Premium Pricing

Suburban markets often provide the ideal balance of moderate competition with relationship-driven pricing. Agents can command $125-200 per signing through consistent quality service and personal relationships with local title companies and real estate professionals.

This is where I found my groove early on. Suburban markets let you build genuine relationships while still maintaining decent volume. You’re not competing solely on price, and you’re not driving 50 miles for every appointment.

The Service Upgrades That Command Premium Rates

Here’s what nobody tells you when you’re starting out: the difference between earning $75 and $200 per signing often comes down to specialized services that create barriers to entry for other agents. After-hours availability, complex document expertise, and premium service packages can dramatically increase your average per-signing income.

I stumbled into this realization when a title company called me on a Saturday evening, desperate for someone to handle an emergency closing. I charged double my normal rate, and they paid without hesitation. That’s when I realized the power of positioning yourself differently.

After-Hours Availability Changes Everything

Agents who make themselves available for evening, weekend, and holiday signings can command 50-100% premium rates. Some earn more in 10-15 weekend hours than full-time agents earn in 40 standard hours, particularly during peak real estate seasons.

According to industry analysis, cutting out the middleman and working directly with escrow officers, loan officers, or real estate agents allows you to keep 100% of the loan signing fee so you get paid up to 50% more for the same exact job. This direct relationship approach becomes even more valuable when offering after-hours services, as clients are willing to pay premium rates for convenience and flexibility.

The notary loan signing agent who answers their phone at 7 PM on a Friday gets the premium work. It’s that simple.

Holiday and Weekend Rate Structures

Developing a premium rate structure for non-standard hours can transform annual income. Peak season holiday signings can command $300-500 per appointment, as borrowers and title companies pay premium rates for convenience and deadline accommodation.

I learned to love holiday weekends once I figured out the pricing structure. While other notary loan signing agent professionals are enjoying their time off, I’m earning premium rates for emergency closings.

| Service Type | Standard Hours Rate | After-Hours Rate | Weekend Rate | Holiday Rate |

|---|---|---|---|---|

| Standard Refi | $100-125 | $150-175 | $175-200 | $250-300 |

| Purchase Closing | $125-150 | $175-225 | $200-250 | $300-400 |

| Commercial Loan | $200-300 | $275-400 | $325-450 | $400-500 |

| Reverse Mortgage | $150-200 | $225-275 | $250-325 | $350-450 |

Specialized Document Expertise Pays Big

Agents who develop expertise in complex transactions face less competition and can command significantly higher fees. Commercial loans, reverse mortgages, and investment property transactions require additional knowledge but offer substantially higher compensation.

The learning curve is steep, but the payoff is worth it. Most loan signing agent professionals stick to residential refinances because they’re comfortable and predictable. That’s exactly why specializing pays so well.

Commercial Loan Specialization

Commercial signings typically pay $200-500 per appointment and require additional training, but the barrier to entry keeps most agents out of this lucrative niche. The complexity and liability involved justify premium pricing for qualified agents.

Marcus, a former bank loan officer turned signing agent, leveraged his commercial lending background to specialize in business acquisition loans and commercial real estate transactions. By obtaining additional certifications and building relationships with commercial lenders, he now handles 8-12 commercial signings monthly at $275-450 each, generating $35,000-55,000 annually from this specialization alone, while maintaining his residential signing business.

The documents are more complex, the stakes are higher, and the borrowers expect expertise. But if you can handle the pressure, the compensation reflects the added value you’re providing.

Reverse Mortgage Certification Premium

Reverse mortgage signings require specialized knowledge but can pay $175-300 per signing with consistent repeat business from specialized lenders. The certification process creates a competitive moat that protects premium pricing.

These signings take longer and require more explanation to borrowers, but the specialized lenders who handle reverse mortgages value reliability and expertise. Once you’re in their network, the work is steady.

Hidden Costs That Are Secretly Killing Your Profits

Most salary discussions focus on gross income without accounting for substantial hidden costs that can reduce effective hourly rates by 40-60%. Vehicle expenses, time inefficiencies, and professional development investments significantly impact your real take-home income.

This is where I made my biggest mistakes early on. I was celebrating $150 signings without calculating what they actually cost me in time and expenses.

One experienced agent shared their detailed analysis: “I found for me… print, prep, travel (×2), sign, scan and FedEx drop … minus expenses I net $30-$40/hr”. This real-world calculation demonstrates how hidden costs and time inefficiencies can dramatically reduce your effective hourly rate from what appears to be lucrative per-signing fees.

When people ask how much does a notary public make, they’re usually thinking about gross fees, not net income after expenses. The difference is substantial.

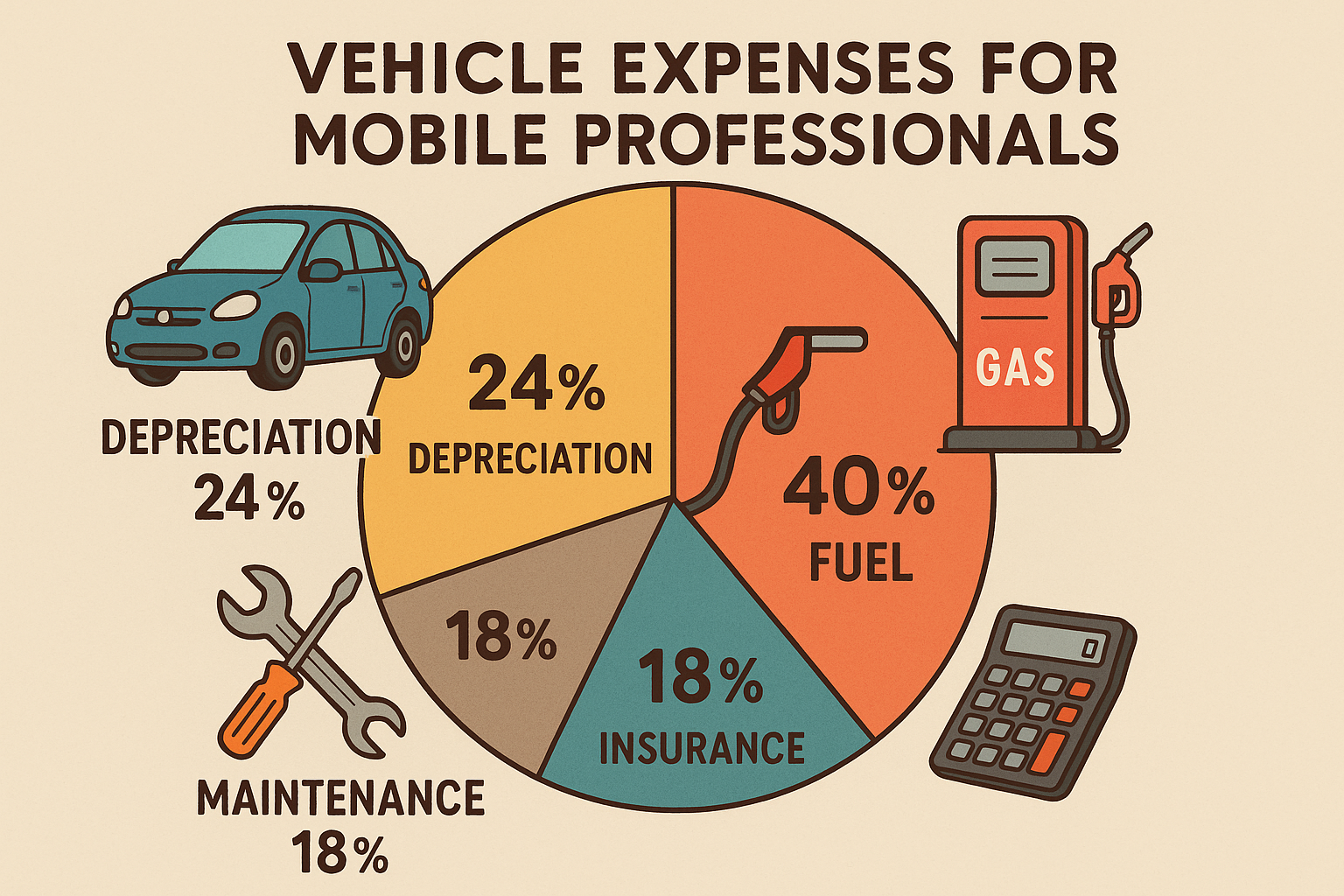

The True Cost of Being Mobile

Vehicle expenses extend far beyond gas and basic maintenance. Accelerated depreciation, increased insurance costs, and the opportunity cost of capital tied up in reliable transportation create hidden expenses that many agents never properly calculate.

I went through two cars in my first three years because I didn’t account for the accelerated wear and tear. Now I budget for vehicle replacement every 4-5 years instead of the typical 8-10.

Hidden Vehicle Cost Calculator:

- Base vehicle payment/depreciation: $300-500/month

- Increased insurance for business use: $50-150/month

- Fuel costs (high-mileage): $200-400/month

- Accelerated maintenance: $100-200/month

- Emergency repairs/downtime: $50-150/month

- Total Monthly Vehicle Cost: $700-1,400

Vehicle Selection Strategy for Maximum ROI

Choosing the right vehicle can impact your bottom line by thousands annually. Hybrid vehicles often provide the best total cost of ownership for high-mileage signing agents, while reliable used vehicles may offer better cash flow than expensive new cars.

I switched to a hybrid after calculating my fuel costs, and it saved me $200+ monthly. The math is straightforward when you’re driving 2,000+ miles per month.

Time Efficiency Reality Check

The time spent traveling between appointments, waiting for borrowers, and handling administrative tasks significantly impacts effective hourly rates. Geographic clustering and efficient scheduling systems can improve hourly earnings by 40-60%.

This was my biggest revelation. I was so focused on booking more signings that I ignored how inefficiently I was scheduling them.

Geographic Clustering That Actually Works

Successful agents develop systems to cluster appointments geographically rather than accepting scattered bookings. This strategy often increases hourly earnings dramatically while reducing vehicle wear and fuel costs.

Jennifer, a Seattle-area signing agent, transformed her business by implementing strict geographic clustering. Instead of accepting scattered appointments across the metro area, she now focuses on 2-3 specific zones per day, completing 4-5 signings within a 15-mile radius. This change increased her effective hourly rate from $25 to $45 while reducing her monthly fuel costs by $300 and vehicle wear significantly.

The discipline required is tough at first. You’ll want to accept every appointment that comes your way, but strategic clustering pays off long-term.

Professional Development Investment Requirements

Maintaining competitive advantage requires ongoing investment in training, certifications, and technology. Professional-grade equipment, continuing education, and technology upgrades represent significant costs that separate successful agents from those struggling with reliability issues.

I budget $3,000-5,000 annually for professional development and equipment upgrades. It sounds expensive until you calculate the income impact of improved efficiency and reliability.

Mobile Office Setup Optimization

Creating an efficient mobile office setup can cost $2,000-5,000 initially but dramatically improves productivity and professional image. Quality printers, scanners, and backup equipment lead to higher fees and more referrals through improved reliability.

Essential Mobile Office Equipment Checklist:

- Portable laser printer with wireless capability ($300-600)

- High-speed scanner or scanner app system ($200-400)

- Backup power bank and car inverter ($150-300)

- Professional document organizer system ($100-200)

- Tablet or laptop for digital processes ($500-1,200)

- Backup equipment for critical components ($400-800)

- Professional carrying case/mobile office setup ($200-500)

Multiple Income Streams Beyond Basic Signings

The highest-earning agents treat their work as a business, implementing multiple revenue streams that provide income stability and growth opportunities. General notary services, corporate accounts, and training income can supplement loan signing revenue significantly.

I discovered this by accident when a local law firm asked if I could handle their regular notary work. That $800 monthly retainer became the foundation that let me be more selective with loan signing appointments.

Expanding Your Notarization Services

Offering general notary services, apostille services, and mobile notary work for businesses provides consistent income between loan signing appointments. Corporate accounts can generate predictable monthly revenue ranging from $500-2,000 per account.

The importance of maintaining proper notary credentials has become increasingly critical as states strengthen their requirements. “Notaries public are appointed by the Pennsylvania Department of State and hold their positions for four-year terms. An application fee of $42 is required, and the processing time for applications generally ranges from 2 to 4 weeks” according to Pennsylvania’s Department of State. This trend toward stricter credentialing creates opportunities for properly certified agents to command premium rates.

The regulatory environment is getting tighter, which actually benefits established notary loan signing agent professionals who maintain proper credentials and professional standards.

Corporate Account Development

Securing contracts with law firms, real estate offices, and financial institutions for regular notary services creates predictable income streams. These relationships often lead to referrals for loan signing work and provide income stability during slow periods.

Corporate clients value reliability over rock-bottom pricing. Once you prove yourself dependable, they’ll often increase your responsibilities and compensation.

Training and Mentorship Income Opportunities

Experienced agents can generate additional income by training new agents, offering consulting services, or creating educational content. This expertise-based income often provides higher hourly rates than signing work while building professional reputation.

I started mentoring new agents informally, then realized I could formalize it into a revenue stream. Teaching others also keeps me sharp on industry changes and best practices.

Advanced Pricing and Negotiation Strategies

Moving beyond standard fee schedules to value-based pricing can dramatically increase average per-signing income. Premium service packages and relationship-based rate escalation allow agents to command higher fees based on reliability and expertise.

Premium Service Package Development

Creating tiered service packages that include same-day availability, detailed borrower communication, and error-free documentation can justify premium pricing of $150-250 per signing. These packages position agents as premium service providers rather than commodities.

Technology That Actually Increases Your Hourly Rate

The most successful loan signing agent professionals leverage technology as a competitive advantage that allows them to handle higher volumes while maintaining premium service quality. Digital workflow optimization and automated systems can increase effective hourly rates by 25-40%.

I was skeptical about technology investments at first. Seemed expensive for someone driving around with paper documents all day. But the efficiency gains are real, and clients notice the professional difference.

Digital Workflow Optimization Systems

Implementing sophisticated digital systems reduces errors, improves efficiency, and creates professional impressions that justify higher fees. Automated scheduling, route optimization, and quality control systems separate top performers from average agents.

The loan signing agent who shows up with a tablet, wireless printer, and digital document management system commands more respect and higher fees than someone fumbling with paper forms and a basic printer.

AI-Powered Appointment Clustering

Using machine learning algorithms to optimize appointment scheduling based on traffic patterns, borrower preferences, and geographic efficiency can add $15,000-25,000 to annual income through improved productivity and reduced travel costs.

Technology ROI Calculator:

- Route optimization software: $50-100/month → Saves 5-10 hours/week

- Automated scheduling system: $100-200/month → Increases booking efficiency 30%

- Digital document management: $75-150/month → Reduces errors by 60%

- CRM system: $50-150/month → Improves client retention 25%

- Total Monthly Investment: $275-600

- Estimated Annual ROI: $8,000-15,000

Client Communication and Retention Technology

Sophisticated CRM systems and automated communication workflows help agents maintain relationships with hundreds of contacts while providing personalized service. This technology enables premium pricing through improved client relationships and referral generation.

I can now maintain meaningful relationships with 200+ contacts without dropping the ball on follow-ups or important dates. The system handles the details while I focus on relationship building.

Automated Follow-Up and Relationship Management

Systematic follow-up with title companies, real estate agents, and borrowers creates professional impressions that lead to referrals and repeat business. Automation allows agents to maintain personal relationships at scale.

Timing the Market for Maximum Annual Earnings

Understanding real estate and lending cycles allows smart agents to maximize income during peak periods while building alternative revenue streams during slower markets. Seasonal patterns create opportunities to earn 40-60% of annual income during peak months.

The income potential becomes clear when analyzing volume requirements: “For that ‘six figures?’ That’s 500 signings per year at $200 a piece (gross) to get $100k. Nobody talks about the hours to achieve that”. This calculation highlights why timing the market and maximizing peak season efficiency is crucial for reaching higher income levels.

When people ask how much do loan signing agents make, the answer depends heavily on whether they’re working smart during peak seasons or just grinding through appointments randomly.

Peak Season Income Maximization

Real estate markets have predictable seasonal patterns that create income opportunities for prepared agents. Spring market preparation and capacity scaling can determine whether an agent earns $60,000 or $120,000 annually.

I learned to think of my business in seasons rather than months. Spring preparation in January and February determines my entire year’s success.

Spring Market Preparation Strategies

Preparing for the spring buying season by building relationships, updating marketing materials, and optimizing capacity determines annual income potential. Agents who scale capacity for peak demand capture maximum income during high-demand periods.

Peak Season Preparation Timeline:

- January: Relationship building and marketing material updates

- February: Capacity planning and equipment upgrades

- March: Staff/contractor network expansion

- April-June: Peak volume execution and quality maintenance

- July-August: Relationship maintenance and process optimization

- September-November: Alternative revenue stream development

- December: Planning and preparation for following year

Economic Downturn Adaptation Strategies

Successful agents develop recession-proof income streams and positioning strategies that maintain income even when loan volumes decline. Understanding interest rate cycles and refinancing waves creates opportunities during economic uncertainty.

The loan signing industry continues to evolve with market demands, as seen in other sectors adapting to economic conditions. “The club made the German see that in January the only possible option would be a loan, although this would also be a remote possibility due to problems with the salary cap” according to Diario Sport. This demonstrates how different industries must adapt their strategies based on economic constraints, similar to how loan signing agents must pivot during market downturns.

Economic cycles are predictable if you pay attention. Interest rate changes create refinancing waves, and smart agents position themselves to capitalize on these patterns.

Refinancing Wave Preparation

Interest rate cycles create predictable refinancing waves that provide substantial income opportunities for positioned agents. Understanding how different rate environments affect loan types allows proactive service and pricing adjustments.

I track interest rate trends and prepare my capacity accordingly. When rates drop, refinancing volume explodes, and prepared agents capture the majority of that business.

How Professional Credibility Impacts Your Fee Negotiations

Professional presentation and credibility directly impact your ability to command premium rates. Having comprehensive documentation of qualifications and certifications can be the difference between securing a $75 signing and a $200 signing, particularly for commercial and specialized opportunities.

When you’re networking with title companies and pursuing higher-paying opportunities, professional documentation of your credentials makes a significant difference. Lost or damaged certificates can undermine your professional presentation just when you need it most.

I learned this lesson when I lost my certification documents right before a major commercial client meeting. The embarrassment cost me a lucrative contract that took months to recover.

ValidGrad’s document replacement services help notary loan signing agent professionals maintain professional credibility by providing backup copies of important certifications and credentials. For agents who have lost notary certificates, training certifications, or educational credentials, this service offers a quick solution to maintain professional presentation materials.

The investment in maintaining professional documentation can pay for itself many times over through increased client confidence and higher fee negotiations. This becomes particularly valuable when pursuing commercial or specialized loan signing opportunities where clients expect comprehensive professional credentials.

Ready to strengthen your professional presentation? Explore ValidGrad’s document services to ensure you never miss out on premium opportunities due to missing credentials.

Final Thoughts

The loan signing agent profession offers genuine opportunities for substantial income, but success requires understanding the hidden economics that most agents never learn. Geographic positioning, service differentiation, and professional systems separate six-figure earners from those struggling to build sustainable businesses.

Your location matters more than your skills in determining base rates, but specialized services and professional presentation can multiply your income regardless of geography. The agents earning $100,000+ annually treat this as a business, not a job – they invest in systems, technology, and professional development that create competitive advantages.

Hidden costs can silently erode your profits if you don’t account for them properly, but smart agents use technology and efficiency systems to maximize their effective hourly rates. The key is understanding that this profession rewards business thinking over simple task completion.

Most importantly, professional credibility and comprehensive documentation of your qualifications directly impact your ability to command premium rates. Whether you’re just starting or looking to scale your existing business, having the right systems and professional presentation in place makes all the difference in your earning potential.